Fast. Free. No impact on credit score.

Home Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

A home loan can have different meanings depending on what you’re looking for, but they generally mean one of the following.

Firstly, it could mean you apply for a home loan to purchase a home or change the existing one you already have on your property. Secondly, there’s borrowing against your home to use its value to pay for something else – like buying a new car or paying off debts. This type of loan is known as a homeowner loan.

Lastly, you can take home loans to mean equity release – a scheme that allows you to refinance your home loan to raise funds in exchange for a percentage of the equity in your home. You can continue living in your home, but it may be partly or completely taken on by the lender when you pass away.

Whether you’re a first-time buyer or looking to purchase a second home, a home loan could be right for you. There’s a range of mortgages available and the type of housing loan that best suits you will depend on your personal situation. Whether you’re a first-time buyer or looking to purchase a second home, a home loan could be right for you. There’s a range of mortgages available and the type that best suits you will depend on your personal situation.

Find out the facts before branching out into second-home mortgages.

Find more information on the homeowner loans Norton offers.

Equity release is a product that can boost the financial prospects of our customers later in life. If you’re 55 or over, you can refinance your home loan by releasing some of the value of the equity on your home.

Equity release allows you to draw a regular source of income or a cash sum from up to 60% of your home’s value. You don’t have to sell your home or even move out if you choose this plan.

With a homeowner loan, you can use your property as collateral to borrow money for purposes such as home improvements, debt consolidation, or other large expenses.

A mortgage is a home loan used to buy a property, but you cannot cover the cost of a deposit with another loan. Borrowing to raise a deposit may affect your ability to secure a mortgage as lenders want to be sure you have the capacity to take on mortgage repayments.

Home loans can fund property purchases, renovations, debt consolidation, or major expenses, secured against equity.

Raise money for any purpose by taking out a second mortgage.

Fund renovations or improvements on your home to increase its value.

Release some of the value of your home as equity to plan for the future or early retirement.

We specialise in helping customers find the home loan that suits them best. That’s because we take into consideration our customers’ individual needs and financial situations.

At Norton Finance, rather than taking a ‘one size fits all’ approach by offering a single home financing product, we scour the market in search of what’s available. This means we can better serve you and offer the service you need.

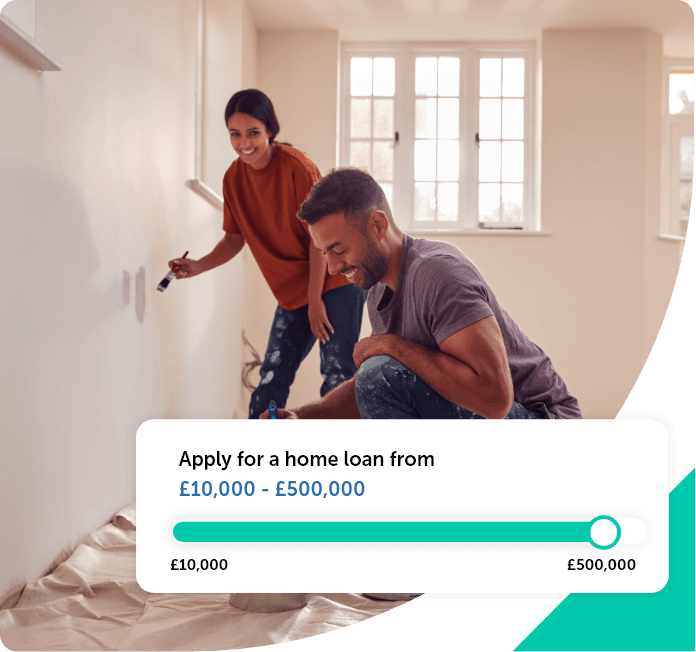

With Norton Finance, you get the flexibility to borrow anything from £3,000 to £500,000, over 1 to 30 years.

We make an ‘in principle’ decision on your application within 24 hours of receiving it. Once a decision is made, you can expect to receive a direct payment in around 14 days.

At Norton, we offer customers flexibility and a straightforward loan process, with access to around 600 products from our panel of expert lenders. We offer plenty of housing loan options around maximum loan amounts and repayment terms, giving you complete control of your finances.

We compare loans rather than offering a single product, and we receive a commission from the lender upon the completion of a loan.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances