Fast. Free. No impact on credit score.

Classic Car Financing

Fast. Free. No impact on credit score.This won’t affect your credit score

As with standard car finance, there are two varieties of classic car loan. The two types include:

With a personal loan, you’ll receive the money up front from a lender. You’ll then have more freedom to shop around for a car of your choosing. You’ll enter a repayment plan with the lender, paying back the loan in instalments.

You can apply to enter a finance agreement with a registered seller. Here, you’ll agree to pay back the loan over a set period of time.

You’ll likely have two options when purchasing a car from a registered car dealer or seller. These are called Personal Contract Purchase (PCP) and Hire Purchase (HP) and both options have different advantages and disadvantages.

You can apply to enter a finance agreement with a registered seller. Here, you’ll agree to pay back the loan over a set period of time. You’ll likely have two options when purchasing a car from a registered car dealer or seller. These are called Personal Contract Purchase (PCP) and Hire Purchase (HP) and both options have different advantages and disadvantages.

With a PCP agreement, you’ll effectively rent the car from the seller. You’ll pay monthly instalments to use the car as your own for a set period, usually a few years. Once this time period is up, you can either buy the car outright for the remaining value owed, called a balloon payment or return the car to the seller.

These agreements can be beneficial if you need to keep your monthly payments to a minimum and don’t plan on owning the car outright, but you are locked into your payments and can usually only drive the car for an agreed amount of miles per year, without paying an additional mileage sum at the end of your agreement.

With a hire purchase agreement, you pay a deposit upfront for the vehicle. You’ll then agree to pay a certain amount per month as part of your contract. Once the full value of your car is paid off, you’ll own it outright.

You won’t be restricted to a certain amount of mileage as with a PCP agreement and you will eventually own the car should you pay off your agreement. However, repayments are generally more expensive.

With a personal loan, you’ll receive the money up front from a lender. You’ll then have more freedom to shop around for a car of your choosing. You’ll enter a repayment plan with the lender, paying back the loan in instalments.

The money you borrow from the lender will either be a secured or an unsecured loan. A secured loan is secured against something you own, usually a house or similar property of high worth. If you default on your loan, the lender can take ownership of your property as payment. An unsecured loan is not secured against anything but tends to have higher monthly payments.

It’s important to remember that purchasing and owning a classic car is an expensive venture. You should be certain you can afford your loan repayments and any insurance you will need for the car before making an agreement with a lender.

If you fail to meet the monthly repayments on a secured loan, you could end up losing your home.

When thinking about applying to borrow, it’s always important to consider your personal situation. You should assess your ability to make monthly repayments as well as the interest fees. This can help you avoid negatively affecting your credit score, and being open to debt collection and court action.

Lenders will consider a number of points when deciding on your loan application. Your eligibility for a loan depends on:

A car can usually be called a classic when it is over 20 years old, at which point it may start appreciating in value. A good low mileage example will generally be worth more than one with high mileage. A classic car value can range from a few hundred pounds up to several million dependent on the make, model and mileage.

Your eligibility for a classic car loan will depend on the requirements of your lender. However, we can help you find a loan that suits your circumstances. We help people from a variety of backgrounds who may not always meet some lenders’ loan criteria, including people with a less than ideal credit history, retirees and the self-employed.

Before applying for a loan, it’s important that you are sure you can comfortably afford the repayments.

We work with a huge variety of lenders to find a financial solution that suits you. If you aren’t deemed eligible by some lenders, we can help you finance that rare find. With flexible repayments and more than 600 loan options, you won’t be stuck on the starting grid with Norton Finance.

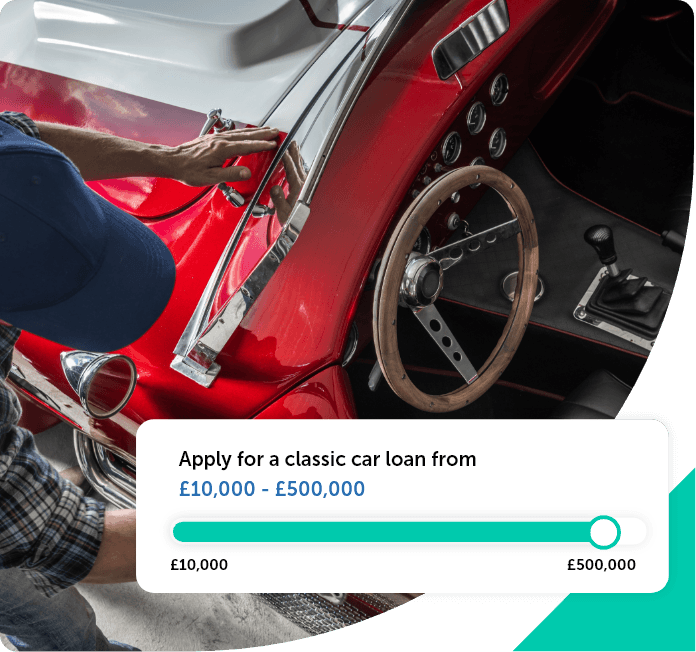

Take a look at our loan calculator to work out your budget for a classic car purchase. Choose the amount you'd like to borrow and for how long to get an idea of the monthly repayments.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

Classic car loans work in much the same way as a loan for a regular car. However, you must specify that you are looking to finance a classic car when applying for your loan, as it will affect the terms of your arrangement with the lender, and how much you are able to borrow.

Otherwise, your vehicle will still be subject to the legal requirement for a yearly MOT to be deemed roadworthy.