Fast. Free. No impact on credit score.

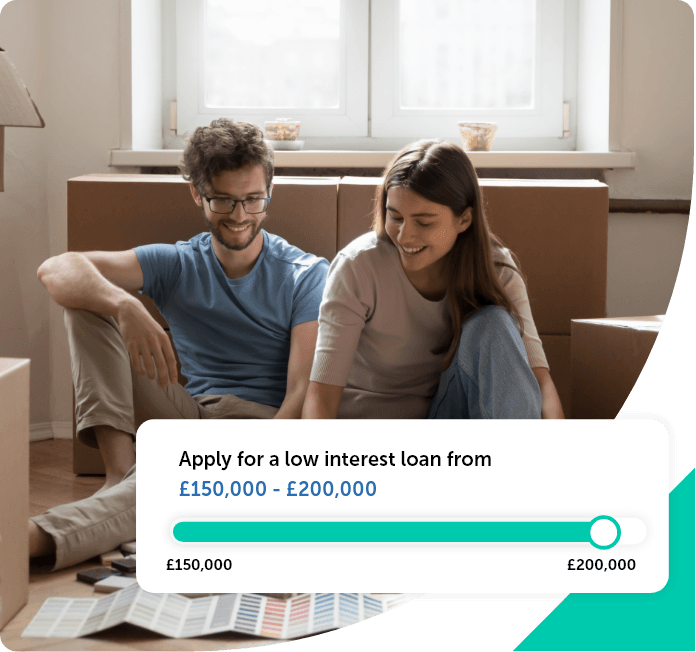

£150,000 - £200,000 Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

Most companies are happy to arrange for you to borrow big loans of up to £200,000 as long as you meet their criteria for lending.

Consider that when applying for a large loan amount like this, the terms of the loan will be set against your property. So, you need to make sure you own enough equity in your home to secure against the £150,000 to £200,000 loan.

It’s important to make sure you can afford the loan in advance and are able to make the repayments on time, as breaking the agreement could put your home at risk.

Before you apply for a £150,000 to £200,000 loan, there are a few things you will need to consider:

Before you apply, you’ll need to calculate your monthly income, regular expenses, and current debts. This will help a lender determine whether you can afford the monthly repayments on a £150,000-£200,000 loan. Lenders will evaluate the source of your income and its stability. If you’re applying to consolidate existing debts, lenders will consider these existing debts and how much they cost you each month.

When applying for a large secured loan, it’s important to evaluate the value of your property. You can calculate the amount of equity in your home (i.e. how much of the property you actually own), by taking the property’s current market value and subtracting the money you still owe towards your mortgage. The more equity you have, the less risk a lender will face, which means potentially better rates.

Lenders will usually check your credit rating before they accept your loan application, so they can see your borrowing history and any county court judgements (CCJs) for debt. It’s useful to be aware of your credit report in advance to answer any concerns or questions the lender may have.

Make sure there’s a clear reason for your loan application as some lenders may have a defined list of acceptable or unacceptable purposes.

You must be a UK resident aged 18+

It’s important to find out the lender’s eligibility criteria when you apply for a loan. This usually varies depending on the loan amount and your financial situation, but generally all loans will require you to be a UK resident aged 18 and over.

Take a look at our article on loan eligibility for further advice on whether you can apply for a £150,000 to £200,000 loan.

As your home will be secured against the loan amount, your credit score isn’t the only factor considered during your application.

Different lenders place different importance on your credit history. Some loan products are designed to help you get your financial situation on track.

But remember, the better your credit score, the lower the interest rate might be.

With large secured loans, it’s better to plan in advance how much you’ll have to pay back and when so you can keep on top of repayments. Not being able to make your repayments on time could have serious consequences, from a negative mark on your credit score to major risks like losing your property.

Our secured loan calculator can provide you with an estimate before you apply to help you determine whether you can afford your desired loan amount.

If you’re looking to raise cash, remortgaging may be an alternative. By remortgaging you can often reduce your monthly repayments and release some of the equity you have in your home to free up the cash.

For further advice and information, take a look at our helpful guide to remortgaging. It highlights the potential benefits of remortgaging, from securing a better interest rate to reducing monthly expenses. It also explores the range of remortgaging products available, so you can see which would work best for you.

With over 50 years of experience, we offer loan plans for individuals seeking to borrow £150,000 to £200,000. Applying for a loan is quick and easy; all you have to do is provide some details regarding your personal and financial circumstances.

Whether it’s your first time applying for a large loan or you’ve been previously turned down, our advisors are happy to share their expertise and help you find the perfect loan for your situation.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

To start your online loan application, you’ll need to provide:

It only takes a few minutes to provide these details. You can use recent bank statements, mortgage statements or payslips to make the process as smooth as possible.

A friendly advisor may also get in touch, so it helps to have further information to hand, such as details of any other debts you may have.