Fast. Free. No impact on credit score.

Car Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

Whether you’re buying your first vehicle or looking to upgrade your current model, Norton Finance will help you find the right loan to finance your next car purchase. We can spread the cost or provide upfront funds if your vehicle has suffered a breakdown or irreparable damage too.

A loan for your car is similar to other personal loans and can be used to cover the cost of a new or used vehicle. Once you receive your loan, you can put the money towards a new or used car, with repayment rates available to suit your requirements, including car finance for bad credit.

Financing a car works in two ways. You can apply for finance with a registered car seller at the time you buy the vehicle and then pay back the loan over an agreed period.

Alternatively, you can apply for a personal loan and receive the money before you shop for a vehicle of your choosing.

By financing a car upfront with a personal loan, you’ll own the vehicle outright. You’ll avoid paying for extras such as excess mileage charges over time, as you may have done if leasing the vehicle from a garage.

However, the monthly payments on your personal car loan could be higher than some other options. So you should be sure you can afford to cover the monthly repayments before you apply.

Our loan calculator is here to help work out if you can get finance for a car. You can work out what your expected monthly repayments might look like by choosing a loan amount and term.

Choosing between a personal or secured car loan depends on your circumstances. If you have a low credit score, you may find it’s difficult to get a personal loan. This is because lenders consider you a higher-risk borrower.

If you find you’re unable to get approved for a personal loan for financing a car, you may prefer a secured loan. This type of loan is secured against an asset, or collateral, such as your home. A secured loan will typically have lower interest rates. But your property may be seized if you are unable to keep up with the loan repayments.

Your eligibility depends on the requirements set out by the lender and will be influenced by your financial history and current situation.

On the other hand, a secured loan could be a better option if you have an asset such as a property or vehicle that can be used as security.

If you have a low credit score, it’s still possible that you could be approved for a personal loan. However, the interest rates for this may be very high and might not suit your budget. In this case, it’s advisable to get in touch with car finance brokers to discuss your personal circumstances and find the best solution.

Our loans can help you afford new car finance, whether you’re a new driver, need an upgraded model or simply want a decent run-around to commute to work. Before you apply, you should look at how much you can comfortably afford to pay back each month.

A loan can be a good way of building credit, improving your rating and your chances of being accepted for better rates in the future.

On top of your loan repayments, remember to factor in the other running costs of having a new or different vehicle, and if you can afford these.

A loan can be a good way of building credit, improving your rating and your chances of being accepted for better rates in the future.

If you’re buying your first car using a loan, you should shop around for some insurance quotes for the type of vehicle you would like to buy. If you are upgrading, things such as the age, make and model, as well as the engine size, can increase insurance costs.

Find out how much tax you will pay on your car beforehand. Car tax rates will vary depending on CO2 emissions and the age of the car. Car finance rates also differ slightly depending on the payment schedule you opt for.

Whether you’re looking to buy a new or used car, it’s likely you will need to pay for maintenance while you own it. Check locally if there are any specialists who deal with the make and model of your car. They’ll offer more competitive rates than servicing directly with the maker’s dealership.

If you are buying a petrol or diesel car, find out what the average MPG for the make and model is so you can estimate fuel costs.

Similarly, if you are looking to purchase an electric vehicle, factor in extra expenditure for the cost per kWh. This may be different if you are charging at home or using a public charging point.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

There are other options to consider when it comes to taking on a loan for a car. You could seek a PCP finance agreement with the dealer, where you take on a loan via their provider.

At the end of your agreement, you have the choice of handing the car back, buying it outright for the remainder of the loan, or swapping it for an even newer model.

You could also consider leasing a car, which may require an initial deposit. Leasing often has lower monthly repayments than a financing agreement, as you’ll only ever cover the depreciating value of the vehicle, rather than the whole cost. The difference is that an initial upfront payment is usually required to agree such terms.

We help people whatever their financial situation and will try to find a car loan for you even if you are retired or self-employed. We also help new drivers who may need help purchasing their first car and those on low-income salaries and apprenticeship schemes who still need a vehicle to get to work and back.

Apply for a loan and you’ll have the freedom to choose your own path towards a new set of wheels:

Drive away in your new car without paying an upfront deposit when you take out a personal car loan.

If you’re buying a car from a private seller, you can borrow the money then transfer directly to them upon agreement of the sale.

A car loan can be used when bidding at auctions, just be sure to only bid up to the amount you have borrowed.

A loan can be used when purchasing pre-owned from a dealer.

Have a question before you apply? We’ve answered some of the most common queries below:

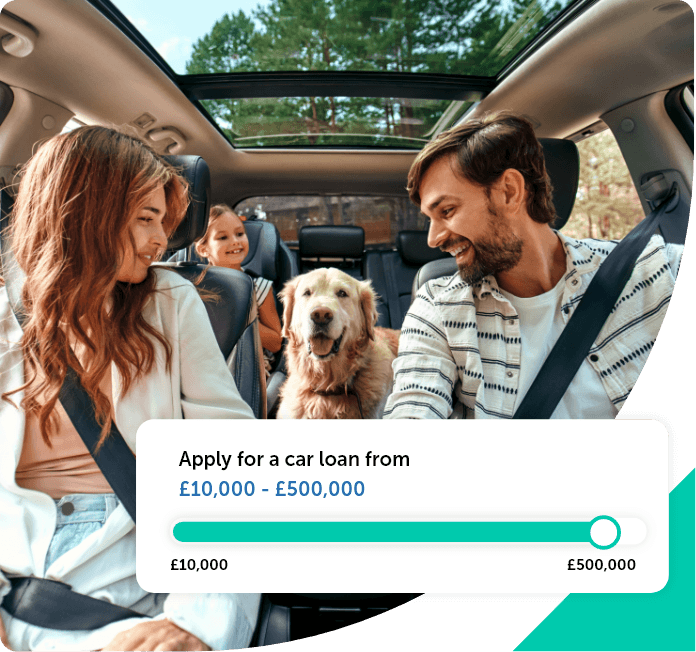

You can apply for a loan between £10,000 and £100,000 - covering a wide range of vehicle options.