Fast. Free. No impact on credit score.

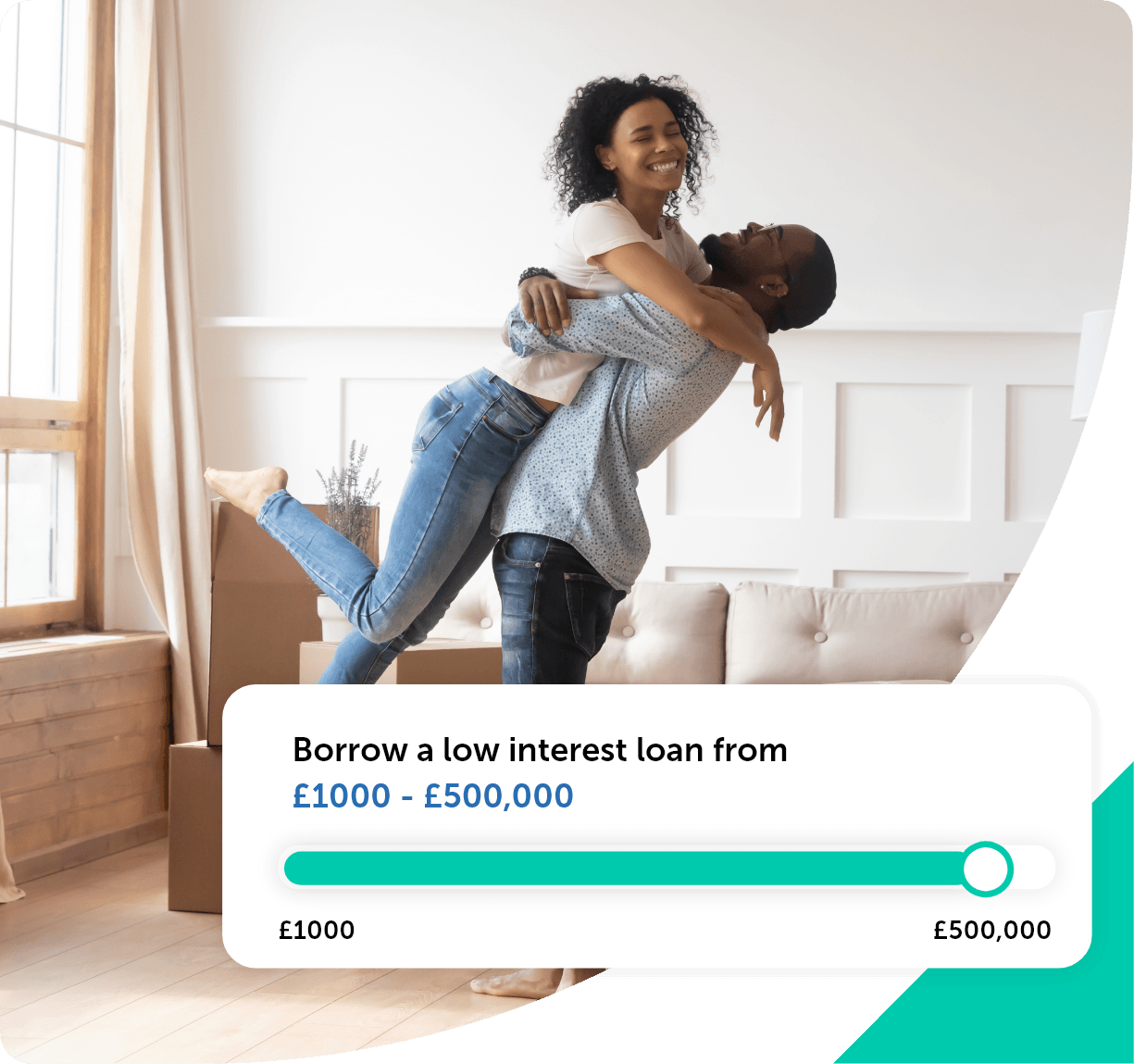

£300,000 - £500,000 loans

Fast. Free. No impact on credit score.This won’t affect your credit score

Most lenders will be willing to approve a loan of £500,000 provided you meet their eligibility requirements – this usually means owning your own home too.

When applying for a large loan amount, the terms of the loan will be set against your property. It’s important to have enough equity in your home to set against a higher-value loan.

Breaking the agreement of a £300,000 to £500,000 loan could put your home at risk. So it’s important you are sure you can make the repayments. The most common ways to borrow this amount of money are via bridging loans and business loans.

A bridging loan is a short term loan which allows you to complete a sale on a property or to clear a mortgage. They should only be used in the short term and taken out with a view to repaying in full as the interest rates associated with a bridging loan can add a lot of interest over time.

If your business qualifies for a loan, then you don’t need to personally qualify for it. This means your own credit score won’t affect whether or not you’re eligible for a business loan. All you need is an established and secure business with a proven track record.

Before you apply for a £300,000 or higher loan, there are quite a few things you need to consider.

If you have a large amount of equity in your home, you’re more likely to qualify for a large loan.

Lenders will assess whether you will be able to make your monthly repayments based on your current financial situation, so it’s important to ensure you know the ins and outs of your budget before you apply.

If you’re looking for £300,000 to £500,000 loan to consolidate debts, this will be taken into consideration - as will the purpose of the loan and the reason why you want to apply for one. It needs to be a suitable purpose to warrant a large loan, so remember to bear this in mind when you apply.

Checking you’re eligible for a loan before you apply is important. To find out more about what you need to be eligible, take a look at our loan eligibility explained guide.

You must be a UK resident aged 18+

With £300,000 to £500,000 loans, you’ll need to have a structured repayment plan so you’re able to keep on top of repayments. Not being able to make your repayments on time could have serious consequences, from lowering your credit score to losing your property secured as collateral on the loan.

Our secured loan calculator can provide you with a repayments estimate before you apply to help you determine whether you can afford to take out a loan of this amount.

Yes, you’ll need a valuation on your property when applying for a large loan amount. Part of the terms for a bridging loan require a valuation so that the lender can assess your property’s suitability and determine an LTV (loan to value) so they will know how much you can borrow.

If you’re looking to raise cash, remortgaging may be an alternative. By remortgaging you can often reduce your monthly repayments and release some of the equity you have in your home to free up the cash.

Remortgaging isn’t suitable for everyone, and it often helps if you are coming to the end of your current mortgage deal. Early repayment fees from your mortgage lender can sometimes make this a more expensive option depending on how long you have left and the terms of your current deal. Learn more about remortgaging in our remortgaging guide.

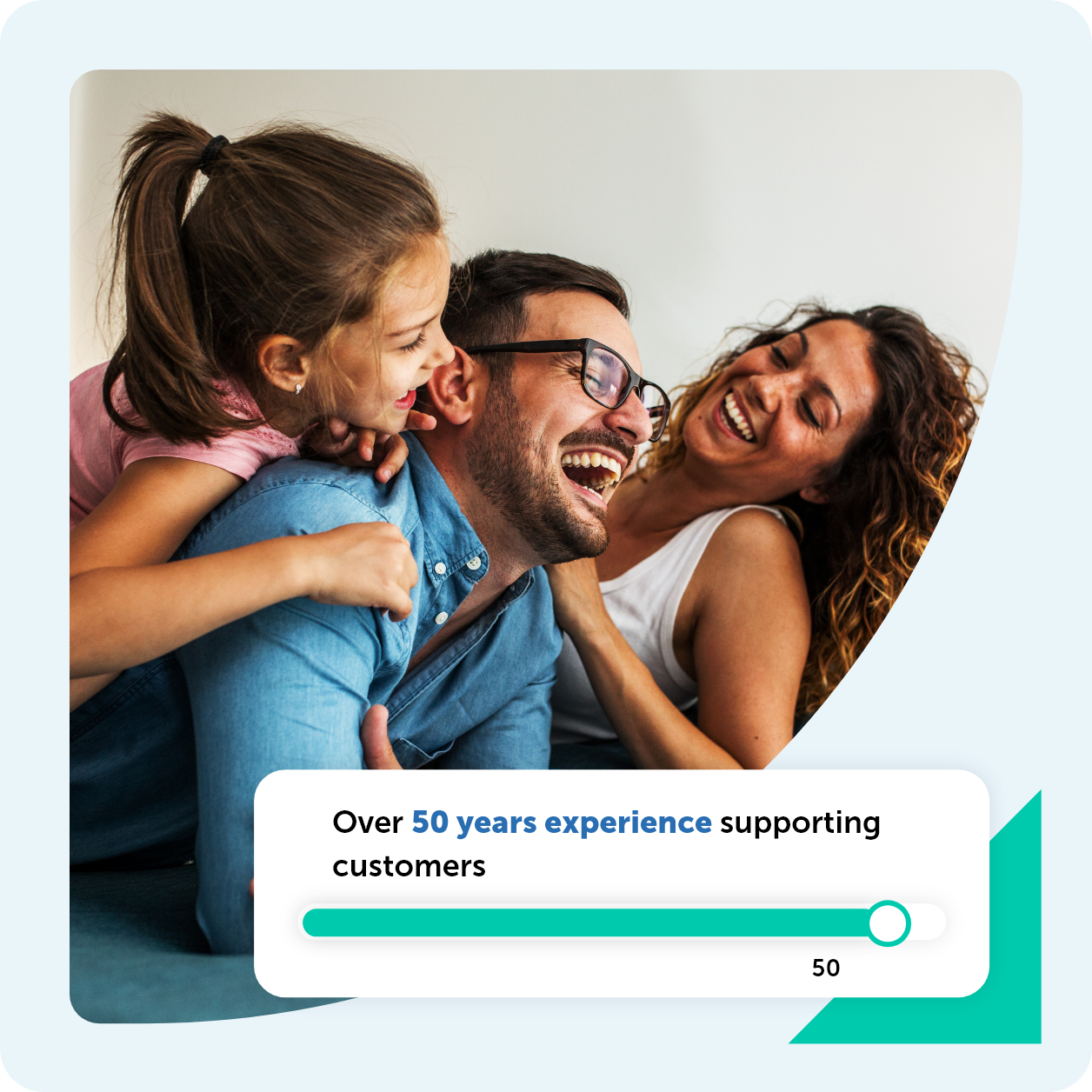

With over 50 years of experience, we offer loan plans for individuals seeking to borrow £300,000 to £500,000. Applying for a loan with us is quick and easy, even if you have been turned away by other lenders in the past.

All you have to do is provide some details regarding your personal and financial circumstances, and our helpful staff will advise you on the next steps.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

You can use personal secured loans for any purpose, but your lender might want to know what your intentions are. People tend to apply with a specific, large project in mind, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Car purchase loans can be cheaper than dealership finance plans, with rates available to suit your requirements.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.