Fast. Free. No impact on credit score.

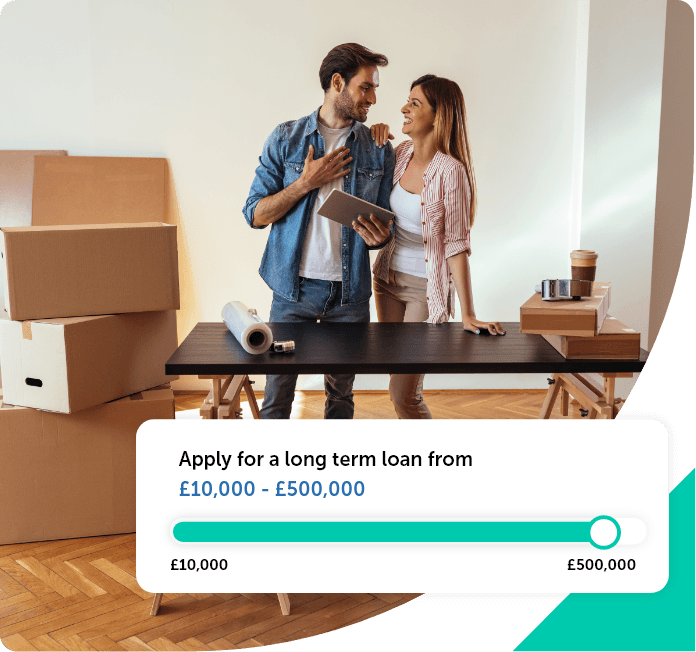

Long Term Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

Long term loans are a form of loan agreement that is typically repaid within a timespan longer than a year. It means you’re able to spread the cost over time, usually at lower interest rates than short term loans.

However, while the repayments are more manageable, overall you’re likely to pay more than short term loans because of the interest payable over a longer term.

Long term loans usually allow you to borrow large amounts of money and then spread the costs into manageable monthly repayments over one to 30 years. They are often offered at a lower APR than short term loans, helping you to manage your finances more effectively.

While the interest rates are lower each month, the longer the terms of your loan, the more interest you will end up paying overall.

Long term loans can also make it tricky to plan for the future, as you still could be paying off your loan in years to come. If you want to pay it off early, you’ll also face an early repayment fee.

The main difference between long term and short term loans is the period over which it is repaid.

A short term loan is often repaid weekly or monthly, over a shorter timescale, while long term loans can span years or even decades. Interest rates are often higher for short term borrowing, while long term loans are designed with a lower rate of interest over a longer period, meaning you may pay a lot more in interest overall.

Which type of loan is more suitable to you depends on your circumstances, so it is important to weigh up the differences before choosing.

You can use personal secured loans for any purpose, but your lender might want to know what your intentions are. People tend to apply with a specific, large project in mind, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Car purchase loans can be cheaper than dealership finance plans, with rates available to suit your requirements.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.

When choosing between a long term and short term loan, it’s important to evaluate what you can afford to pay back, over a repayment period that suits you.

With long term loans, lenders may pay closer attention to your credit rating to understand your financial circumstances and make a decision of whether you can afford the repayments in one, two or even ten years’ time. Therefore, make sure your credit report is up to date and without errors before applying.

You can start your application for a long term loan online with just a few details to hand, including:

We will then get in touch to discuss your requirements, so it’s a good idea to have information handy regarding what you need the loan for, and whether you are taking out a loan to consolidate debts.

Our online secured loan calculator is also useful to get an idea of how much you can borrow for a long term loan.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

Try to choose a loan amount which is affordable, at a repayment period which suits your situation, both now and in the future.

As we are a broker, not a bank, we search across the market from over 600 different loan products to find the best fit for you. We receive commission from the lender on completion of a loan application, and we may also charge a broker fee of up to 12.5% of any secured loan amount borrowed, capped at £3,995. There are no broker fees on unsecured loans.