Fast. Free. No impact on credit score.

Remortgage your house with us

Fast. Free. No impact on credit score.This won’t affect your credit score

Remortgaging is when you replace your existing mortgage plan with new terms. It could help you find a better deal and reduce your monthly mortgage payments, while also freeing up funds for home improvements or life’s important moments – like a wedding.

There are several reasons to remortgage, from homeowners who’ve seen an increase in market value to those looking to improve their home.

If your property is worth more now, considering your mortgage repayments against the estimate increase, you may want to renegotiate the terms of your mortgage.

Before looking into this, it’s worth knowing your equity.

When applying for a remortgage, it’s worth knowing your equity, for example:

You can use this equity value to calculate your loan-to-value rate (LTV), which is given as a percentage. A lower LTV rate can be a great way to secure lower interest rates on your remortgage deal. This may mean:

The alternative is to borrow more money than you currently owe against the value of your home. You’ll receive the difference as a lump sum in your bank account to use for your chosen purpose.

There are alternatives though, and remortgaging doesn’t always rely on increases in market value. Whether it’s for a holiday, home renovation, or your business, there’s options to suit you.

For more information, read our guide to remortgaging to release equity in your home.

Remortgaging is about using your current financial situation to save money on mortgage repayments or raise some much-needed cash as a lump sum.

You’ll benefit from applying for a remortgage if your financial situation is improving. However, if your home has decreased in value or your credit report has been negatively impacted, you could end up paying more per month than you set out to.

Before you apply, check out our guide on what you need to know before remortgaging.

Your eligibility for a remortgage depends on a few factors such as:

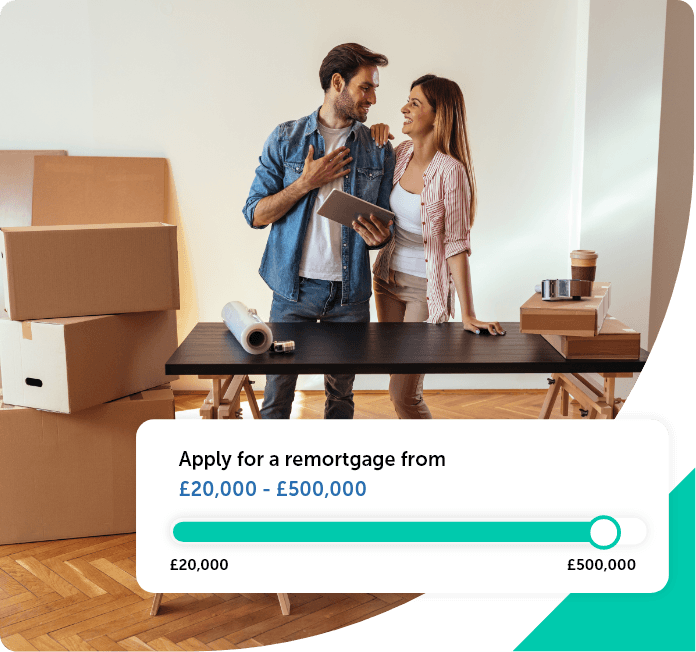

These factors can also determine how much you can borrow. With Norton Finance, this could vary anywhere between £5,000 to £500,000.

Lenders have their own criteria when deciding your remortgage terms, but by working with a wide range of lenders we can try to find a loan that suits your specific circumstances.

Before committing to a remortgage, ensure you can afford any new repayments or fees. For more advice, visit our guide to remortgaging with bad credit.

You can use a remortgage for any purpose, but your lender might want to know what your intentions are. People tend to apply with a specific, large project in mind, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Car purchase loans can be cheaper than dealership finance plans, with rates available to suit your requirements.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.

There may be fees involved when it comes to remortgaging. The process often requires contractual changes, so it’s important to consider these before deciding whether to remortgage.

Switching lenders could incur an early repayment charge if you’re still fixed into a deal, meaning you must pay your old lender for moving your mortgage. For example, a fixed rate mortgage will normally have an early repayment charge if you repay or change your mortgage during the initial fixed-rate period.

Some mortgages may have administration charges to consider, including booking, valuation, and conveyancing costs. Not all lenders will charge these, but you may want to look into it before making any commitments. When you apply for a remortgage with us, we’ll make clear all the possible fees you could face at each stage of the remortgage process.

Like any important decision in life, you should weigh up the pros and cons of remortgaging before making the big commitment.

Whether it’s increasing the resale value of your property with a new extension or financing a wedding, you can free up funds against your property, giving you a lump sum to spend as you need.

With property values increasing over time, your home may be worth more than when you bought it. By getting a remortgage quote, you can often find a much cheaper rate, meaning you could potentially save on the interest you’re paying.

When switching lenders, you may have to pay your original lender a penalty fee. This is called an Early Repayment Charge. Not all mortgages have Early Repayment Charges - it will depend on the type of product you have - so it’s important to see whether any potential costs outweigh the benefits you’ll get from any cash sum or new repayment plan.

If you’ve only just purchased your home or don’t have much equity invested yet, it’s unlikely you’ll find a better rate. You may find it’s worth waiting until you’ve paid off more of your mortgage before considering a switch.

There are different types of remortgage loan, so see below to help you decide which one is right for you:

Click apply for a remortgage to start your journey

Fill out our online form for your personalised rates

Get the remortgage that best suits your circumstances