Fast. Free. No impact on credit score.

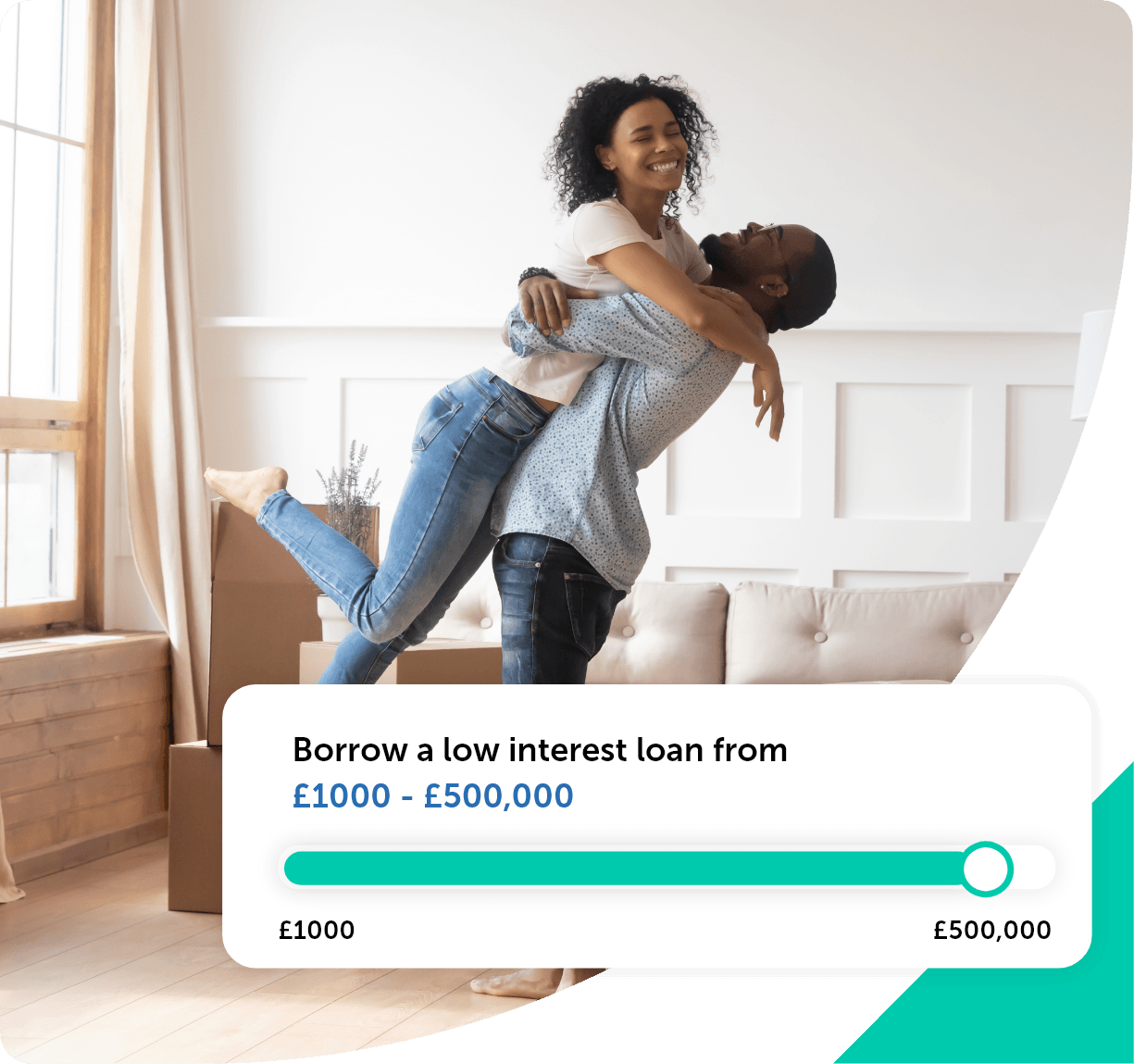

£60,000 – £100,000 Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

Even when choosing to accept £60,000 to £100,000 loans, you can expect lenders are willing to work with you to find the most suitable loan product. Due to the larger amounts in question, applicants will need to own enough equity in their home that they can borrow against.

Your credit score is just one of the factors which lenders look at to see how you manage credit. However, it isn’t the only thing they consider for your application. Demonstrating that you have a good record of repaying loans on time is just as important as having a good credit score. For loans up to £100,000 the amount of equity you own is arguably a more important factor than your credit score.

Equity is the amount of property you own. If you have a mortgage, your equity is the current market value minus what you still owe to your mortgage provider.

Your credit history shows when you’ve borrowed money and paid it back – as well as when you haven’t. Your credit score isn’t the only thing lenders consider.

You should look at your income and outgoings to determine your budget, and therefore how much you can put aside for regular repayments.

You should have a specific reason for borrowing the money. Lenders may not accept a loan application for certain reasons.

You won’t know for sure if you are eligible for a £60k loan or more until you apply, but you can get a good idea about how likely you are to be accepted by reading our tips on eligibility.

Before committing to a loan, it’s essential that you understand the proposed fees, rates and repayments and ensure you can afford to borrow. Our loan calculator is a really useful tool for working out how much you’ll be expected to pay back on your loan before you accept an offer of a loan.

When it comes to creating a repayment plan you can use our repayment calculator:

Use the slider on the loan calculator to find the best fit for your repayment schedule.

To fill in a standard loan application form, you will need to provide some basic information about yourself and your circumstances. These should include your:

If you plan to use your loan to consolidate other debt repayments, please have details on those arrangements to hand. This will make the process much easier as it gives lenders all the information they need to arrange payment.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

However, as a bridging loan is a short-term product you may find interest rates are higher than other types of loan, due to the amounts involved.

It isn’t recommended you take out the loan unless you are confident of paying back the loan in full, sooner rather than later.

Our homeowner rates start at 5.39%. We take your financial history and present circumstances into account, so the interest rates we offer can vary.

If you have any other questions, get in touch with a member of our team and we’ll do what we can to help.

You can use personal secured loans for any purpose, but your lender might want to know what your intentions are. People tend to apply with a specific, large project in mind, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Car purchase loans can be cheaper than dealership finance plans, with rates available to suit your requirements.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.