Fast. Free. No impact on credit score.

Loans for Debt Consolidation

Fast. Free. No impact on credit score.This won’t affect your credit score

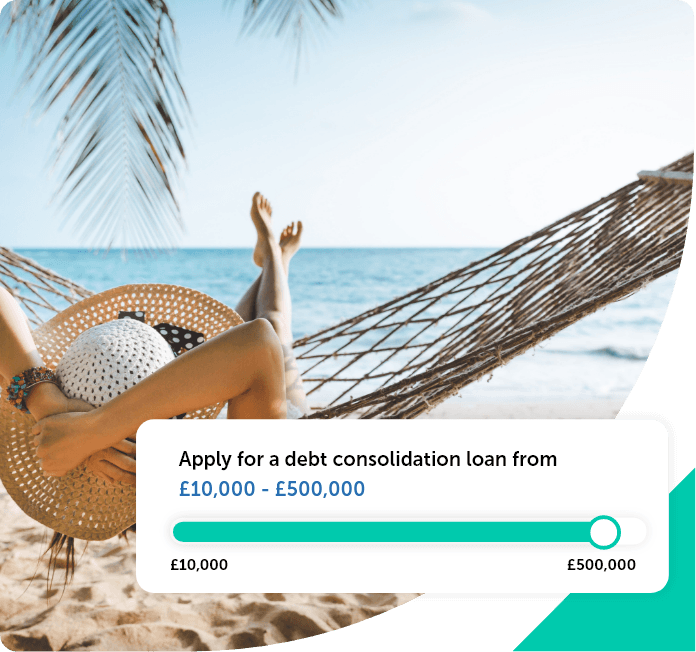

A debt consolidation loan can help you take control of your finances by combining credit cards, personal loans or home loans into one fixed monthly repayment. Instead of juggling multiple payments and interest rates, you’ll deal with just one lender and one repayment plan, making it easier to budget and manage your debts.

When it comes to consolidating home loans and loans in general, there are two main types to consider – secured and unsecured.

Before you take out a debt consolidation loan, it’s important to do your research. Borrowing money can give you access to the funds you need to pay off your debts but it means you need to be confident you can make monthly repayments towards paying off the loan. A debt consolidation loan can help you take control of your finances by bringing multiple repayments into one. But before applying, it’s important to feel confident you can manage the monthly payments comfortably.

Not every situation requires the same kind of loan. There are two types of loans available, each with unique features to suit different circumstances.

A secured loan is where you borrow money secured against an asset –usually your home. If you don’t keep up with your repayments, you may lose the asset you used to secure the loan.

With an unsecured loan, sometimes known as a personal loan, the money you can borrow is determined by your credit score. It won’t be secured to any of your assets in the way a secured loan is.

The process for consolidating existing loans will be similar, no matter the type of loan. Fully understanding your debts before you apply can help us determine your eligibility for certain deals.

Consolidation loans are a way to combine all debts into one payment. This makes it easier to manage and oversee your debts while taking positive steps towards improving your financial circumstances. You can usually consolidate all types of debt, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.

By consolidating home loans and other personal loans, you could lower the overall interest rate from the individual loans. This should make it easier to pay off your debts faster.

If you have a poor credit score, it can be difficult to access competitive deals for financial borrowing. You may also find it challenging to access the credit limit you require. This is because lenders see you as a risky option.

When searching for consolidation loans with bad credit, a secured loan could raise your chances of a successful application. With secured loans a home, or a property you own, is used as ‘security’. Think carefully about this option – if you fail to make repayments, your home or car could be repossessed.

Unsecured consolidation loans are still a possibility if you have poor credit. However, it could be difficult to find the credit limit and interest rates that suit your financial circumstance.

There are a few ways you can prepare before you apply to give yourself the best chance of being approved. This can include:

SECURED LOANS - Rates start at 6.59% variable. We also have a range of plans with rates up to 36.6%, giving us the flexibility to help you find a loan that suits your needs.

If you borrow £34,480 over 10 years, initially on a fixed rate for 5 years at 7.60% and for the remaining 5 years on the lenders standard variable rate of 8.10%, you will make 60 monthly payments of £467.50 and 60 monthly payments of £473.06.

The total repayable would be £56,528.60 ( This includes a lender fee of £595 and a broker fee of £4137) The overall cost for comparison is 11.3% APRC representative.

The maximum APR is 36.6%.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

When you start an application online, our team will be in touch over the phone to talk through a few details. We’ll ask for further information about you, such as:

We may also discuss your current situation and the existing debts you have. This helps us search the market for the best loan for you and check your debt consolidation loans eligibility.

Before you start, it’s best to make sure you have details on any outstanding amounts to hand, along with your current loan terms, monthly payments, and interest rates. By providing this information you’ll help us to better understand your situation. We can assess your debt consolidation loan eligibility and see if we can help simplify your finances by offering a loan that would lower your monthly repayment amount.

Use our debt consolidation loan calculator to help you determine what kind of monthly repayments you might expect to make.

You will qualify for a debt consolidation loan if you are approved for a new loan of an amount that enables you to pay back at least two existing debts. Debt consolidation loan eligibility is assessed in a new credit application and will be accepted based on your credit score and circumstances.

If you have a poor credit score, it can be difficult to access competitive deals for financial borrowing. You may also find it challenging to access the credit limit you require. This is because lenders see you as a risky option.

When searching for consolidation loans with bad credit, a secured loan could raise your chances of a successful application. With secured loans a home, or a property you own, is used as ‘security’. Think carefully about this option – if you fail to make repayments, your home or car could be repossessed.

Unsecured consolidation loans are still a possibility if you have poor credit. However, it could be difficult to find the credit limit and interest rates that suit your financial circumstance.

If you think you might need a break from repayments at any point, you should check the terms before applying. While some lenders do offer ‘payment holidays’ on loans for debt consolidation, these can show up as a negative on your credit report.

Also, be aware that if credit is repaid by a consolidation loan over a longer term, the amount repayable may be higher.

Applying for any form of credit could mean a temporary decrease in your credit score, especially where multiple searches have been placed on your credit file.

However, taking out a debt consolidation loan in particular doesn’t negatively impact your overall credit score. In fact, over time it could act as a boost as you make repayments and prove your reliability as a borrower.

Just make sure to keep on top of making payments regularly. If you're concerned about any negative implications, it's important to seek advice from one of our experts beforehand.

Unlike a secured loan, an unsecured debt consolidation loan (also known as a personal loan) isn’t linked to any property you hold. That means, if you fall behind in payments, a lender won’t be able to take ownership of your property.

Debt consolidation without the risk of losing your property may instead be subject to higher rates.

We can give you the tools you need to better manage your financial situation, by offering a simple and flexible loan process. Our team can assist you in every way possible to ensure you get the repayment terms and interest rates that are best for you.

Once we’ve received your application, we’ll make an ‘in principle’ decision within 24 hours. We can also make direct payments around 14 days after your application has been approved.