Fast. Free. No impact on credit score.

Bad Credit Remortgages

Fast. Free. No impact on credit score.This won’t affect your credit score

Trying to arrange finance such as a remortgage with bad credit history can be difficult. If your credit score has been affected by falling behind on mortgage or loan repayments, you may have been refused elsewhere. A bad credit remortgage can help reshape your month-to-month situation.

We source remortgages from a comprehensive list of lenders to help those with bad credit history, and our expert team is on hand to advise and assist you through every stage of the process.

Yes, many lenders will work with you to find a remortgage product that’s suitable for you even if you have bad credit. You may not have as many to choose from, but it’s not impossible to find a loan to suit your circumstances.

Bad credit remortgage loans may be offered with higher interest rates. This allows lenders to offset the risk when it comes to your credit rating.

If you need quick results, opting for a product with a higher rate may be best. However, this will result in higher monthly repayments where the money used on the interest rate may have been better put towards the balance.

But, if you can improve your credit score, you’ll benefit from reduced interest rates and more remortgaging options.

Some lenders won't approve applications for remortgage because of a borrower’s poor credit history, as it means there’s a higher chance that you won’t be able to afford the repayments in the long run. While this is incredibly frustrating, there are a few things you can do to improve your credit score before applying for your remortgage.

You can repair your history of adverse credit by getting back on track and creating a pattern of regular payments. You can also do simple things like making sure you’re enrolled on the electoral register and using your credit card for small items that you pay back straight away.

Find out more about getting your credit score in good shape on our Know How blog.

When it comes to getting a remortgage with poor credit, there's much to consider. It's because of this that we've tried to create a process that's as simple as possible for all homeowners.

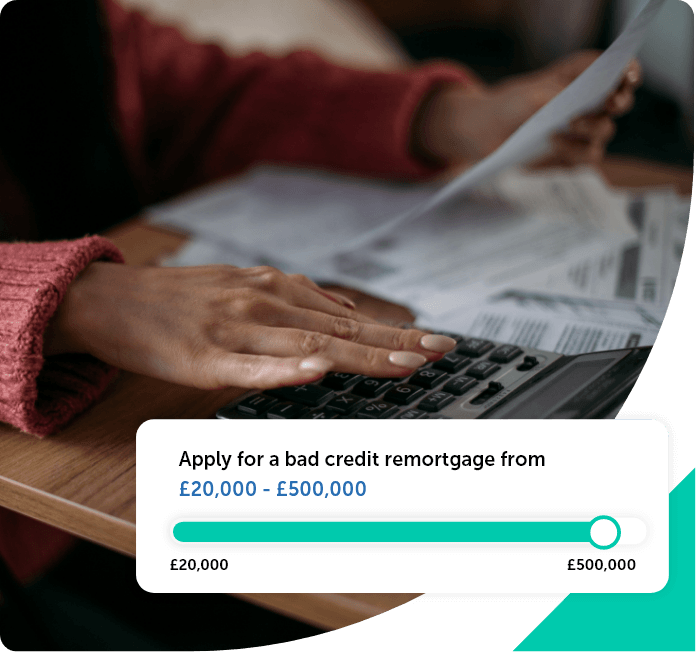

First figure out how much you'd like to borrow, then use our straightforward remortgage calculator at the top of this page. This will help you come to a decision as to whether remortgaging is what you need.

After we've collected all your details, we'll help you navigate the next steps.

Click apply for a remortgage to start your journey

Fill out our online form for your personalised rates

Get the remortgage that best suits your circumstances

In terms of your credit rating, taking out an additional mortgage doesn’t necessarily impact your credit score. Most lenders run soft searches on your credit history at the application stage, which doesn’t affect your credit score even if you make more than one application at a time.

If you are thinking of applying for a second mortgage, you must be sure you can afford the repayments, as taking further unaffordable credit is likely to harm your credit score.

For more on the different types of credit search, see our guide.