Fast. Free. No impact on credit score.

Equity Release Remortgages

Fast. Free. No impact on credit score.This won’t affect your credit score

If you’re aged over 55 and own your own home, you could apply for an equity release mortgage. However, you should be aware of the requirements you’ll need to fulfil to be eligible.

Your eligibility depends on several factors, including:

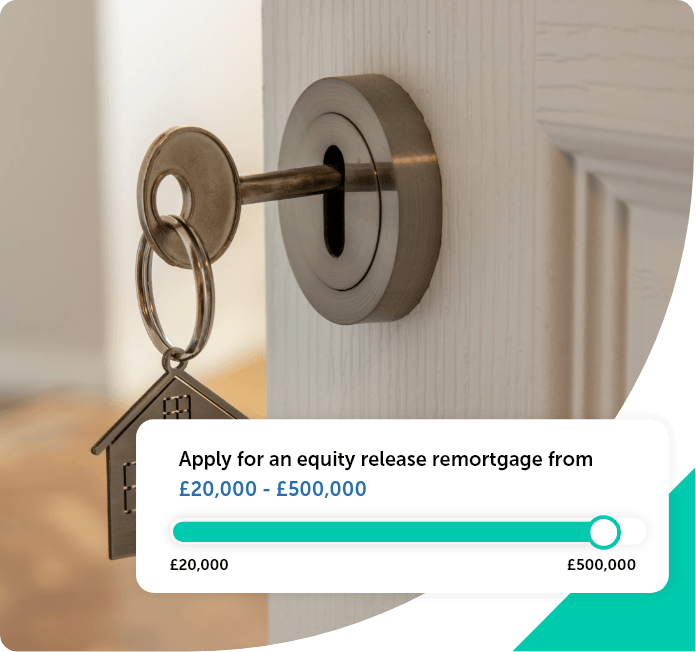

You can release equity in one lump sum, or over several instalments if you’d prefer to receive payment over time. However, you will pay interest on each of the smaller sums.

Before releasing equity from your home, it’s important to receive professional advice from a financial advisor so you fully understand the process and can decide if it’s right for you.

You can release equity in one lump sum, or over several instalments if you’d prefer to receive payment over time. However, you will pay interest on each of the smaller sums.

Before releasing equity from your home, it’s important to receive professional advice from a financial advisor so you fully understand the process and can decide if it’s right for you.

There are two different types of equity release for your property - lifetime and home reversion. Each has its own features, benefits and things to be aware of. Read more about equity release.

Releasing equity as a lump sum is a form of lifetime mortgage agreement. You’ll usually receive your finances in one go. However, this arrangement also comes with compound interest. This means the outstanding balance can grow larger than it would with other kinds of loan.

You may choose a lump sum equity release, as payments don’t need to be made until the house is sold, although some options may allow you to make repayments rather than let the interest roll up.

A home reversion equity release plan allows you to sell either the entirety or a portion of your property at a below market value. The home reversion plan is generally only available to homeowners aged 65 and over.

You can either receive the funds in a lump sum or through regular payments. After the sale, you’ll then be able to live in the house rent-free. At the end of the plan, your property is sold and the sale proceeds are shared according to the remaining proportions of ownership.

Click apply for a remortgage to start your journey

Fill out our online form for your personalised rates

Get the remortgage that best suits your circumstances

As with all types of remortgage, equity release has its benefits and drawbacks, so there are some things to take into account before you apply. For many, it can be an effective way to borrow, but it’s important to consider whether it’s right for you.

Benefits of equity release include:

As with any financial decision, it’s important to be aware of the disadvantages before making any commitments. These can include:

When it comes to drawing an equity release mortgage, there are a lot of financial aspects to consider. We want to make it easy for you to find out what you need to know.

Once you have decided how much you want to borrow, you can use our online application to apply. We can then put you in touch with one of our specialist providers, who will work with you to decide whether an equity release scheme meets your needs and circumstances.

You can use a an equity release remortgage for any purpose, but your lender might want to know what your intentions are. People tend to apply with a specific, large project in mind, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Car purchase loans can be cheaper than dealership finance plans, with rates available to suit your requirements.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.

Releasing equity from your home is a big financial decision, so it’s important to be aware of every factor involved. Here are some of the most common queries around equity release.