Fast. Free. No impact on credit score.

Home Improvement Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

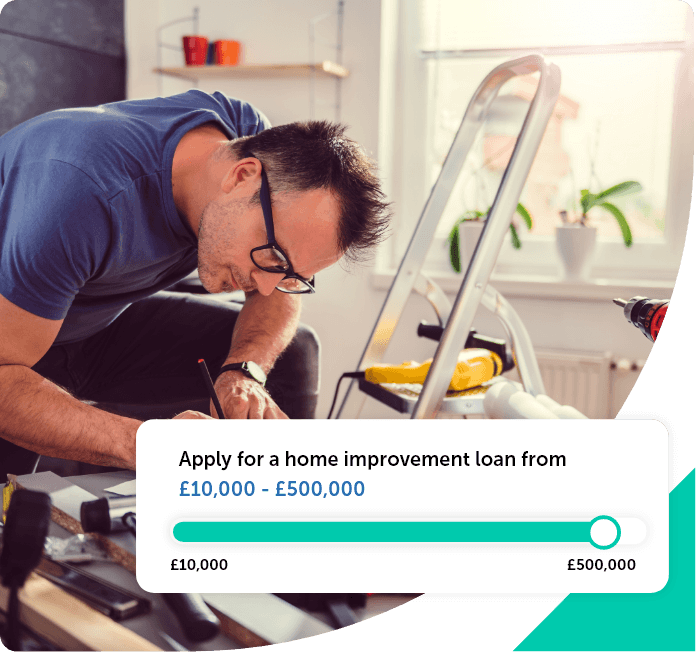

A home improvement loan is a personal loan that’s used to update, improve and renovate your property. Repayments can be spread over a period of time that works for you. Many people find this type of loan can help cover the cost of larger refurbishment jobs.

Possible lenders offer a choice of secured loans or unsecured loans renovation loans, providing a choice for your personal situation. However, it’s important to remember that there are risks associated with both. Secured loans will offerlower interest rates, but your home will be at risk if you fail to meet repayments. And while unsecured loans are not secured against your assets, lenders can start collection or court action if you fail to pay.

If you're thinking of investing your time and money into a home improvement, it's important to weigh up the pros and cons of the process to make an informed and responsible decision.

Loans for home improvement can ensure you have the funds to renovate your home upfront. This could help cover the initial outlay you need in order to cover the expenses of renovation and any building work.

You’ll get a fixed rate on repayments, which means you’ll have a clear idea of how much you can expect to pay back over time and per month.

If you take out a secured loan, you must ensure you can keep up with the repayment schedule. Consistently missing payments could put your home or other assets at risk and lead to court action and

Every lender has their own criteria, including your income, credit score, equity, and loan amount. For more details, visit our guide to county court judgements (CCJs), as well as impacting your credit score.

If you apply for an unsecured home improvement loan, your payments could end up being higher. This may mean you have cashflow problems if renovations end up becoming more costly than you anticipated - for example, if building work runs on longer than planned.

Your home improvement loan can be used for several different renovations or refurbishment works in your household – however large or small.

You could borrow to pay for building works associated with adding a new garage.

Finance any electrical and plumbing work and help cover the material and labour costs.

Create a whole new space for you and your family to enjoy with a loft conversion.

Pay for building materials and any labour expenses associated with adding an extension to your home.

secured loans and unsecured loans for home improvement provide borrowers with a choice of how they want to obtain funds upfront.

If you own your home, or have assets you could use as collateral, a secured loan can work out cheaper in the long term than unsecured loans. This is down to typically better interest rates and larger amounts available.

However, an unsecured loan doesn't require any assets as collateral. If you have a strong credit rating, you may be considered a lower risk by lenders. This means that you don't need the security of an asset to support your loan application.

At Norton Finance, we’ll work with you to find a lender that offers the loan you need at an affordable rate.

Discover more about our loan eligibility criteria in our guide.

When you start your online application, we’ll contact you to get a few simple details from you. We’ll ask for your:

We’ll also discuss what specific home improvements you’re looking to make to your property. Plus, we need to gather a little information about your house itself – as this will help us find the best option for you.

We try to make the contact process as smooth as possible. However, if you have a few details about your current financial situation with you, you can make it even easier. Any recent bank or mortgage statements and payslips can help you answer our queries quicker.

At Norton Finance, we can help you find a home improvement loan to suit your personal financial status and renovation needs. As Norton is a broker, not a bank, we can search the full market to get you the right deal.

We have access to over 600 plans, which can let you borrow between £3,000 and £500,000. Loan periods range from between one to 30 years, adding some flexibility to your plans.

Use our loan calculator to get an idea of the monthly repayments by choosing your preferred loan amount and term.

You’ll receive an instant decision on your loan in principle. However, you should allow between seven to 14 days for your application to be processed and the money to be transferred to your bank account.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

Work out what you can realistically afford to repay each month and see if there’s a loan that matches your repayment budget. Some lenders let you spread the repayments over as much as 30 years, but remember, this will mean you end up paying back more in the long run. Whatever the timeframe, it’s very important that you’re in a financial position to comfortably meet the repayments set out by the lender.