Fast. Free. No impact on credit score.

Unsecured Loans

Fast. Free. No impact on credit score.This won’t affect your credit score

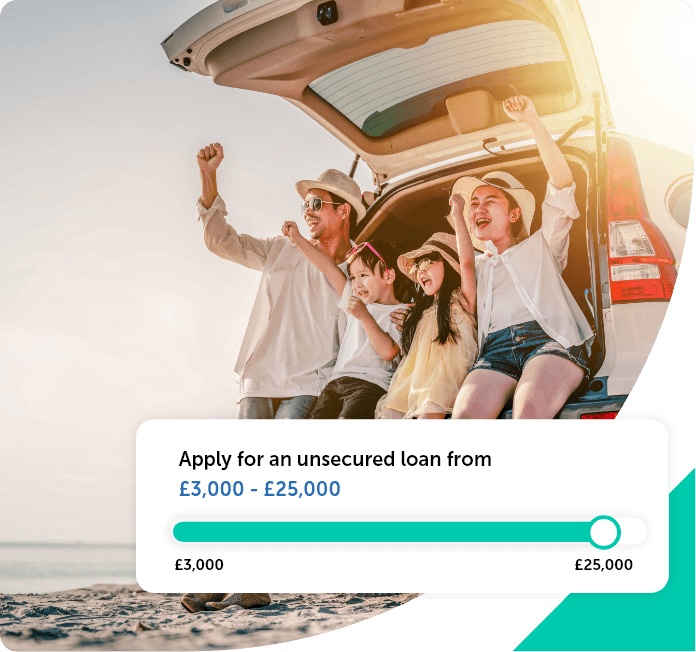

This type of loan is an agreement between the lender and a borrower that is not secured against property, which allows you to borrow from £3,000 to £25,000. It’s different to a secured loan, which you might take out against your property or car.

With unsecured borrowing, your chosen lender will approve the loan, which you pay back with interest over an agreed time period.

Unsecured borrowing can mean higher rates because the lender feels there is a higher risk without using property as a guarantee. However, it can be a useful and efficient option if you do not have property to secure your borrowing against, and can be quicker to arrange.

If you can’t keep up with repayments, the borrower can’t claim against your home or car. Instead, the lender could take you to court, where you may be liable to a County Court Judgement (CCJ) or debt collection. Before you borrow, you may want to plan out a monthly budget which includes your repayments to reduce the chances of this happening.

Before you take out a unsecured loan, it’s important to do your research. Borrowing money can give you access to the funds you need to pay off debts or make a big purchase. But, it means you need to be confident you can make monthly repayments towards paying off the loan. Before you take out a unsecured loan, it’s important to do your research. Borrowing money can give you access to the funds you need to pay off debts or make a big purchase. But, it means you need to be confident you can make monthly repayments towards paying off the loan.

Not every situation requires the same kind of loan. There are two types of loans available, each with unique features to suit different circumstances.

A secured loan is where you borrow money secured against an asset –usually your home. If you don’t keep up with your repayments, you may lose the asset you used to secure the loan.

With an unsecured loan, sometimes known as a personal loan, the money you can borrow is determined by your credit score. It won’t be secured to any of your assets in the way a secured loan is.

When thinking about applying to borrow, it’s always important to consider your personal situation. You should assess your ability to make monthly repayments as well as the interest fees. This can help you avoid negatively affecting your credit score, and being open to debt collection and court action.

Lenders will consider a number of points when deciding on your loan application. Your eligibility for a loan depends on:

You can use personal unsecured loans for any purpose, but your lender might want to know what your intentions are. People tend to apply with a specific, large project in mind, such as:

Borrow to raise the funds for the materials you need to redecorate, or build an extension.

Car purchase loans can be cheaper than dealership finance plans, with rates available to suit your requirements.

Save on fees and hassle by clearing other existing debts, in favour of a single monthly repayment, with a debt consolidation loan.

Give your start-up a boost or grow your customer base. Business loans can help give you the edge over your competitors.

Before applying for an unsecured loan, it’s worth understanding what lenders look for. These factors affect how much you can borrow and whether your application is approved.

Lenders will assess your income and outgoings to ensure you can afford the monthly repayments. They may also ask about any existing debts.

Lenders will use your credit report to determine your suitability for a loan. For this reason, it’s important to make sure your report is accurate. Any errors in the information you provide such as your address or income could affect the chances of your application’s success.

You don’t need perfect credit, but lenders will check your history, including any missed payments or CCJs. A stronger credit profile could help you access more competitive deals.

It’s also helpful to have a clear loan purpose in mind, as some lenders have restrictions on what their secured loans can be used for.

Every lender has their own criteria, including your income, credit score, equity, and loan amount. For more details, visit our guide to loan eligibility.

Applying for a loan with Norton Finance is easy and hassle-free. Simply:

At Norton Finance, we can help find a loan that suits your needs as compare hundreds of loan options, not just one like a bank or building society.

You could borrow between £3,000 and £500,000, over 1 to 30 years, depending on what works best for you. Unsure of how much you can afford to borrow? Try our secured loan calculator.

You can get a decision in principle within 24 hours and if approved, the money is usually paid within 14 days.

Click apply for a loan to start your journey

Fill out our online form for your personalised rates

Get the loan that best suits your circumstances

When applying for unsecured borrowing, you will need to provide the following:

Once you’ve supplied these, we’ll be in touch to talk through the next steps.

Ahead of our introductory call, it can be helpful to have your financial records handy, such as bank statements, monthly income and mortgage or rent payments.

If you’re planning to use your loan for debt consolidation, you can help speed up the process by gathering the information you have about any other existing loans or credit cards, including repayment costs and loan periods.

Stay on top of payments and the loan won’t negatively affect your credit rating.

On the other hand, hard searches are visible and may negatively affect your credit score if they lead to unsuccessful loan applications.

If you have multiple loans, it’s also worth noting that lenders will be able to see this on your credit report and may opt not to lend you more money if the perceived risk is high.

Norton Finance can help find a loan that corresponds to your personal financial situation and your individual needs. Because we compare loans, rather than offering one product like a building society or bank, we can scour the full market and identify the right loan for you.

We’ll likely also discuss what you plan to use the loan for. Most importantly, we’ll need to gather some information about your home. You would only qualify for a secured loan if you’re a homeowner.

TWe’ll make an ‘in principle’ decision on your application within 24 hours of receiving it and can make a direct payment in around 14 days. Use our unsecured loan calculator on this page to find out how much and for how long you can afford to borrow, adjusting the sliders to meet your ideal terms.

At Norton Finance, we have access to over 600 loan products as well as flexible repayment plans.