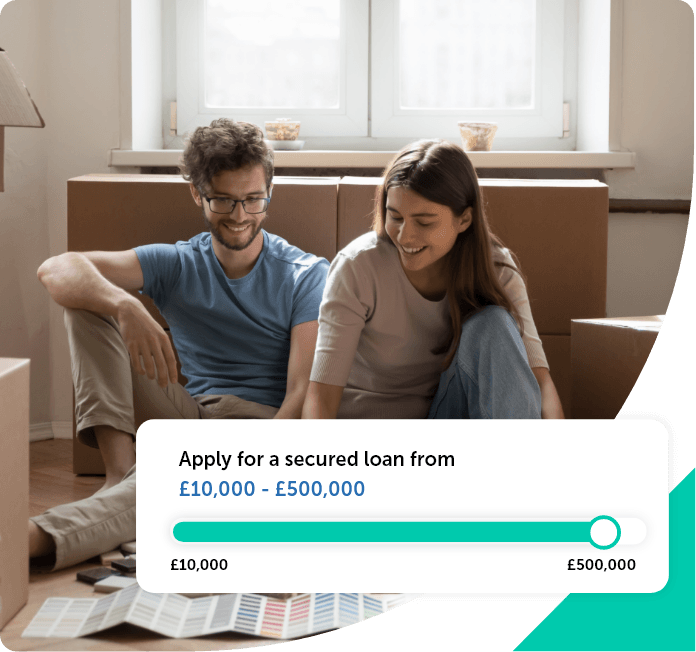

What to consider before taking out a secured loan.

“Like any form of borrowing, secured loans have pros and cons. The key factor here is that the loan is secured against your property, so lenders are often more willing to offer higher loan amounts than with an unsecured loan.”

“That said, it’s vital to be sure you can afford the repayments. If you fall behind on your payments, your home may be at risk of repossession.”

Lisa Muscroft

Head of Loans Broking at Norton Finance

Specialist in secured lending and complex cases, with extensive experience supporting customers across complex borrowing scenarios.